How many energy communities exist in Spain? Who is leading the charge? And what can the Spanish market learn from the Austrian model?

In this article, we explore the current state of energy communities in Spain, upcoming regulatory changes, and lessons from European markets. The new framework for collective self-consumption is opening a much broader market: energy retailers can create higher-retention energy products around local generation, while IPPs, renewable developers, asset owners and municipalities can turn solar, storage and flexible demand into locally differentiated offers.

Energy communities in Spain are no longer a niche concept. As renewable energy costs continue to fall, battery storage becomes more affordable, and the regulatory framework evolves, the conditions for large-scale adoption are rapidly improving.

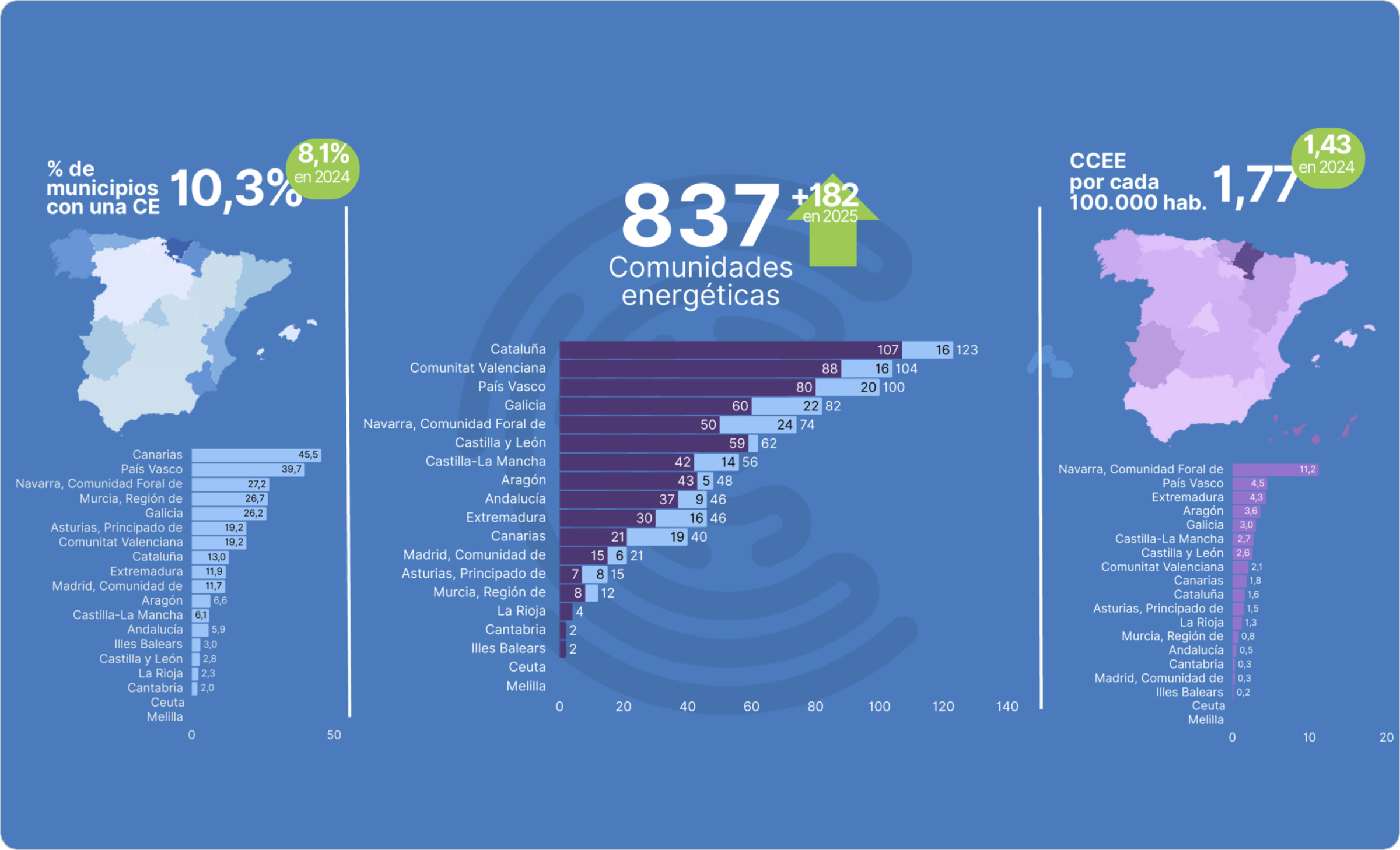

According to the latest Energy Communities Observatory published by ECODES, Spain had 837 energy communities operating in 2025, demonstrating steady growth across the country. At the same time, recent regulatory developments are expanding the possibilities for collective self-consumption, energy sharing, and community-led renewable energy projects.

But while regulation creates the opportunity, scaling energy communities requires much more than legislation. Successful projects depend on data management, participant onboarding, energy allocation, billing processes, and seamless collaboration between distributors, utilities and energy retailers, IPPs and renewable developers, municipalities, and community managers.

The third edition of the Energy Communities Observatory, developed by ECODES through its Energía Común initiative, provides one of the most comprehensive snapshots of Spain's community energy landscape. By 2025:

Beyond renewable energy generation, many communities are pursuing broader social goals, including energy affordability, vulnerable consumer participation, gender equality, and local economic development.

This highlights an important reality: energy communities are not only an energy transition tool – they are also a mechanism for strengthening local resilience and social inclusion.

For utilities and project developers, these figures point to an important market transition as well. Spain is moving from early-stage, grant-supported initiatives toward projects that need repeatable commercial models: participant acquisition, long-term asset utilisation, transparent settlement, customer support and integration with retail energy contracts. Collective self-consumption is likely to be the most immediate route to scale, because it can be deployed without requiring every project to first establish a full energy-community legal structure.

The growth of energy communities is not happening in a vacuum. Three converging factors are opening a window of opportunity that did not exist a few years ago:

Price volatility and negative-price hours. Spain's high solar penetration has widened the gap between peak and off-peak prices and generated an increasing number of hours with negative wholesale prices. This creates a structurally favourable environment for local self-consumption and demand flexibility.

Rapidly falling storage costs. Battery system costs dropped 27% between 2024 and 2025. This is fuelling a new wave of projects and making shared storage models economically viable at scales that were not feasible until recently.

Regulation moving in the right direction. Spain is putting in place regulatory developments that, while still incomplete, are converging toward the models that have proven to work in more mature European markets.

It is worth clarifying a distinction that matters operationally: collective self-consumption is a technical and economic sharing arrangement that does not require a formal legal entity. An energy community, by contrast, is a legal entity with open and voluntary membership, democratic governance and a local purpose. The recent regulatory changes primarily affect collective self-consumption, while the legal framework for energy communities continues to evolve.

The most significant changes introduced by RDL 7/2026:

The proposed update to RD 244/2019, whose public consultation has closed and which remains pending approval, contains elements that could significantly change how collective self-consumption operates day to day.

Austria is currently the benchmark market for energy communities in Europe. The numbers make the case: more than 10,000 active communities, growing at a rate of 200 to 400 new communities per month, with over 300,000 supply points enrolled – representing between 6% and 8% of all supply points in the country.

What did Austria do differently? Four factors explain the success:

1. Model flexibility. Austria recognises several distinct typologies: neighbour self-consumption (building level), local renewable energy communities, regional communities and national communities. Each model addresses different needs. An industrial generator with plants in multiple cities can use the national model to share surplus between sites; a rural community fits better within the local framework. The existence of multiple models removes the need for every project to fit the same mould.

2. Economically grounded incentives. Local communities pay no taxes on the kilowatt-hours shared, and grid tariff discounts reach up to 64% for local communities and up to 28–64% for regional ones depending on voltage level. The technical rationale is straightforward: if generation happens close to consumption, fewer sections of the high-voltage network are used. The discount reflects real infrastructure savings rather than being a subsidy.

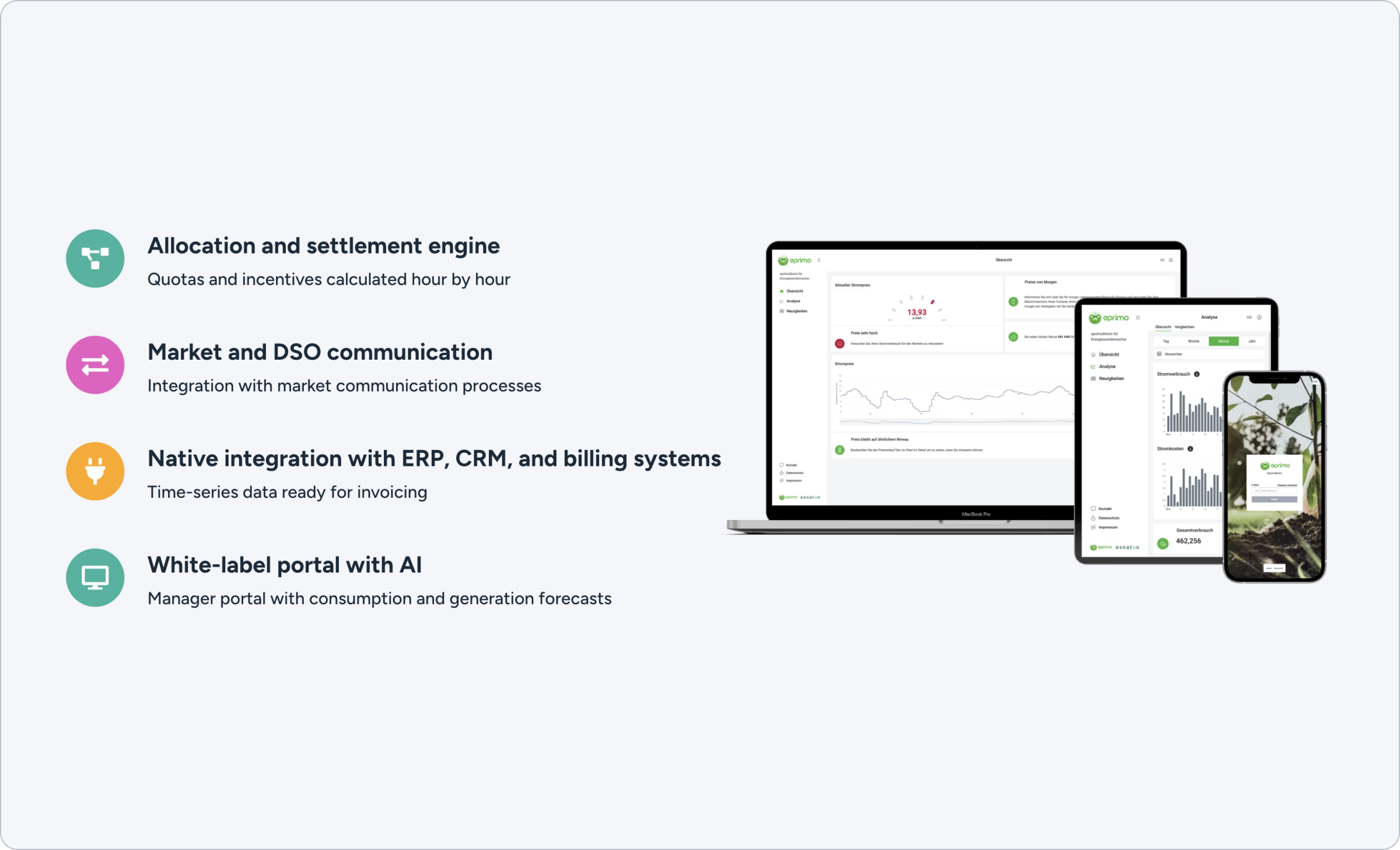

3. Mature digital infrastructure. The EDA (Energie Daten Austria), operational since 2012, is a regulated data hub for energy data exchange between all market participants. exnaton connects to the EDA via API and receives – following end-customer consent – all metering data from the previous day at 15-minute resolution. That data forms the basis for calculating sharing coefficients, issuing invoices and displaying consumption in near-real time. Without this infrastructure, managing 10,000 communities efficiently would simply not be possible.

4. Institutional support and mediation. When energy community regulation came into force in 2021, Austria simultaneously established the Koordinierungsstelle – a national coordination office that provides free guidance, templates and practical support, and acts as mediator between distribution network operators (who are not always aligned with new regulations) and community promoters.

One of the clearest lessons from the European markets where exnaton operates is that regulation creates the right, but data quality, data governance and processes with the distributor determine whether that right is actually scalable.

The case of Kelag – one of Austria's three largest energy retailers – illustrates this well. Kelag uses exnaton's platform to manage its energy communities and neighbour self-consumption schemes, covering everything from digitised onboarding through to billing, the customer portal and bidirectional SAP integration.

What started as a relatively simple integration five years ago has had to evolve into a more fully automated system as volume grew. Member onboarding, metering data validation, sharing coefficient calculation, billing based on actual quarter-hourly consumption and customer-facing visualisation are all processes that can be handled manually at small scale. At hundreds or thousands of communities, they cannot.

The customer portal in this case goes beyond displaying data. Members can see how much of their consumption comes from the community versus the grid – and, in one of the most illustrative examples of where the sector is heading, they can charge their electric vehicle using community surplus, with a price signal derived from a 48-hour production forecast sent automatically to the vehicle. The goal is not just visibility but actionable flexibility: directing consumption to the hours when local energy is most abundant.

Energy communities are not merely a regulatory compliance exercise or a social initiative. For energy retailers, they represent a concrete strategic opportunity:

Customer retention. A retailer that manages a customer's energy community creates a deeper, more embedded customer relationship that can improve retention and reduce reliance on price-only competition. Retaining an existing customer consistently costs less than acquiring a new one, and energy communities deepen that retention significantly.

Revenue diversification. Beyond the margin on kilowatt-hours sold, managing flexibility – storage, electric vehicles, demand response – opens new service lines that commodity retail does not.

First-mover positioning. The energy sector has demonstrated repeatedly that actors who resist structural shifts eventually cede ground to those who embrace them early. The photovoltaic rollout followed this pattern. Energy communities are likely to follow the same trajectory.

Asset monetisation and route-to-market for IPPs. Local energy products can reduce dependence on a single revenue stream by combining asset output with customer acquisition, local consumption, storage and value-added services. The opportunity is strongest where renewable assets, nearby demand and a credible retail or operating partner can be brought together.

Spain enters 2026 with 837 energy communities, an accelerating regulatory framework and a market that is beginning to have clear reference points – both in its own data and in proven European models. The technical and economic conditions are aligned: falling solar and storage costs, price volatility that incentivises local generation and regulation that is, step by step, moving toward dynamic coefficients, shared storage and simplified administrative processes.

What will separate the organisations that lead this market from those that fall behind will not only be the ability to sign up members. It will be the capacity to operate communities at scale efficiently: reliable data, automated processes with distributors, accurate sharing calculations and a customer experience that makes the value of participation tangible.

For utilities, IPPs, developers and municipalities, the next question is not whether shared self-consumption will grow in Spain. It is which projects can become repeatable, profitable products – and what operating model is required before scale creates complexity.

exnaton helps energy companies turn local generation, storage and flexible demand into operational energy products: from participant onboarding and allocation to settlement, billing, customer experience and integration with existing IT systems.

Are you a utility, energy retailer, IPP, renewable developer or municipality evaluating a shared self-consumption or energy-community product in Spain? Let’s assess the operational model, regulatory fit and route to market together.